Last year was a challenging year for the floating production systems (FPS) market. The low oil price threatened the commerciality of numerous projects, delay announcements for FPS units under construction arrived regularly and overall only four orders were placed. So far in 2016, Douglas-Westwood is reporting a similar trend, or arguably worse market conditions. No orders have been placed this year and a number of projects – such as the Vette FPSO – have been cancelled.

Last year was a challenging year for the floating production systems (FPS) market. The low oil price threatened the commerciality of numerous projects, delay announcements for FPS units under construction arrived regularly and overall only four orders were placed. So far in 2016, Douglas-Westwood is reporting a similar trend, or arguably worse market conditions. No orders have been placed this year and a number of projects – such as the Vette FPSO – have been cancelled.

Despite these problems, there is light at the end of the tunnel and 2H 2016 should see improvement.

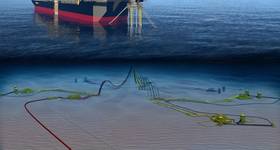

“This is expected as a consequence of improving oil prices, cheaper shipyard/module fabrication costs and re-engineered projects. FPS units that should be ordered this year include; an FPSS for Mad Dog Phase 2 in the US Gulf of Mexico and an FPSO for the Madura MDA/MBH project in Indonesia,” Douglas-Westwood said.

According to the firm, expenditure on installations in the sector is expected to remain high and Douglas-Westwood forecasts spend of US$58 billion on FPS units 2016-2020 – a 32% increase over the hindcast. Much of this capital expenditure (capex) is for units ordered before the oil price collapse with sustained high oil prices leading to the sanctioning of high capex FPS units.

Douglas-Westwood believes that the majority of spend will be in traditional high-capex regions of Latin America and Africa which account for 33% and 22% respectively. However, beyond these regions, spend will be diverse with Western Europe, North America, Asia and Australasia each seeing over 8% of total capex. FPSOs will continue to represent the largest segment of the market with 79% of capex, TLPs and FPSS’ will account for 9% and 10% of capex respectively while spars will account for 2%.

Despite the current lack of orders, there are still near-record backlogs to be worked through, ensuring shipyards remain active. The speed with which new orders arrive will be important and we anticipate that the first order will likely lead to a spurt of other orders, as many operators wait for costs to bottom-out before ordering. Consequently, the next few years represent a major opportunity for operators to capitalize on lower costs, while also providing manufacturers with the opportunity to move towards standardization as the industry focuses on cutting costs. What will be vital is ensuring that the lessons learned are not forgotten should there be an unexpected increase in the oil price.

Image of Mad Dog, from BP.

Subscribe

Subscribe