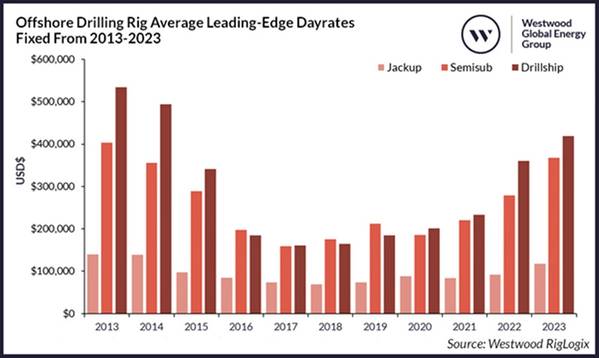

The price to rent an offshore rig hit a nine-year high last year with jackups, semisubmersibles and drillships costing on average $118,000, $368,000 and $419,000, respectively (as of 31 December 2023). These figures represent an overall 54% increase in dayrates when compared with 2021.

This swift rate of cost inflation – sparked by higher global rig demand, rising utilisation and tightening availability – has more recently become a factor in the slowdown in contracting activity as operators take stock of their current rig provisions and look at ways to keep future projects economical, as well as being extra careful to make the right rig selection, especially for long-term campaigns.

One potential solution, as demonstrated by a recently struck deal between TotalEnergies and Vantage Drilling, is to acquire a majority stake in a rig. Specifically, ultra-deepwater 7th generation drillship Tungsten Explorer, for which the operator is to purchase a 75% stake through creation of a new joint venture (JV) with the drilling contractor that will retain the remaining 25% interest in the 2013-built rig. As part of the deal, TotalEnergies will pay $199 million and Vantage will continue to manage the rig for 10 years.

TotalEnergies Chairman and CEO, Patrick Pouyanne, stated that the deal was done to help control costs as rig dayrates continue upwards. The operator also commented that the effective dayrate for the rig will be “much lower than $400,000”, which is around the current average price per day for a rig of this calibre. Pouyanne also stated that the JV will provide “value and flexibility” and hinted that more such deals are to be expected from the company in the future.

Back in June last year, the operator issued a tender in search of two ultra-deepwater drillships for up to 10 years apiece, with one rig to be solely placed offshore Angola while the other unit would move between various countries including Angola, Mozambique, Namibia and Suriname to cover exploration and development activities.

With the first deal awarded, rumours are rife that a similar ownership agreement could be struck for the operator’s second requirement.

Previous Agreements with Mixed Success

While the deal is certainly one of a kind, this is not the first time an operator has opted to buy or at least acquire a partial stake in an offshore rig in a bid to control costs and availability. In fact, joint drilling contractor and oil company rig ownership dates back to the 1970s, but oil companies eventually decided they did not want to be in the rig owning business and most partnerships were dissolved.

Some of the more recent examples include Brazilian National Oil Company (NOC) Petrobras and Mitsui JV – P&M Drilling International, which owns the ultra-deepwater drillship Petrobras 10000. Transocean manages the rig, which has been working for Petrobras since its delivery in 2009, and it has an agreement in place with P&M to acquire the rig under a 20-year capital lease contract.

In addition to Petrobras, there are other NOCs that have owned fleets at their disposal. ONGC is a good example, as it currently owns and operates six jackups and two drillships in addition to the 34 rigs it rents from other rig owners.

Meanwhile, Shell and Noble jointly designed ultra-deepwater drillships Noble Bully 1 and 2, which were both delivered in 2011 at a cost of $600 million apiece but only worked for the operator for five and seven years respectively, before the pair were retired in 2020 and 2021 due to limited success with the ship’s design. The Bully rig design featured a compact box-type drilling tower, known as a multi-purpose tower, instead of a conventional derrick.

In addition, two Cat-J jackups Askepott and Askeladden are owned by the Norwegian Oseberg and Gullfaks licence holders (both licences are operated by Equinor). The two rigs, managed by KCA Deutag, are being used for exploration and development drilling within the offshore licences and were specifically designed to suit Equinor’s requirements at the fields. The pair were delivered in 2017 and 2018, respectively.

Another E&P company that bent on ensuring its rig supply is U.S.-based Arena Energy. Arena has set up multiple affiliates to manage various activities, including a group of companies that operate under the White Fleet umbrella, one of which is White Fleet Drilling (WFD). WFD was created in 2017 and was established to secure jackup services in the wake of the shrinking local rig supply, as well as fewer contractors. The company currently owns three jackups – WFD 250, WFD 350, and WFD 400. When operating, the rigs are managed by Enterprise Offshore Drilling. A fourth unit, WFD 300, was retired upon purchase of WFD 400 in 2022. All of these jackups were previously owned by other rig contractors. While these units are primarily for use by Arena Offshore, they have, from time to time, been leased to other U.S.-Gulf operators. As of March 2024, two of the five jackups working in the U.S. Gulf are WFD rigs working for Arena Energy affiliate Arena Offshore.

Who Else Could Look to Buy?

It may not be the first time we have witnessed an operator buying a stake in a rig, but it certainly is the first time in almost a decade, which is a sign of the times in the ongoing rig market recovery. But will we see more operators jump on the bandwagon?

It is unlikely, as was the case in the previous market upcycle, that this will become a common trend. However, for those operators with the need to secure long-term capacity of over 10 years it could be a solution to help control project economics.

As it currently stands, outside of TotalEnergies’ second drillship requirement, there are no other known outstanding 10-year (or longer) duration tenders in the market. However, a few supermajors as well as NOCs have several three-to-five-year requirements for jackups and floating rigs currently at a pre-tender, tender or direct negotiation stage, though this is likely not long enough to warrant taking a stake in a rig.

In addition, a drilling contractor must be interested in taking part in such a deal, so what is in it for them? Vantage Drilling CEO Ihab Toma commented that “the proceeds from the sale of the Tungsten Explorer will completely deleverage our balance sheet while putting in place a meaningful, long-term revenue stream leveraging our strong management expertise.”

Not only did Vantage secure almost $200 million in cash, it also locked in a substantial flow of long-term revenue for the company, which is also rumoured to be gearing up for a potential sale. Meanwhile, TotalEnergies will benefit from the drilling contractor’s ongoing management expertise.

To conclude, it is unsurprising in this current market upcycle that some operators are considering ‘out-of-the-box’ ways to keep rig costs down and secure the right assets for future projects. While unlikely to become a common trend, and depending on how the market performs over the next few years, we may see a few others follow in TotalEnergies’ footsteps.

Subscribe

Subscribe