Despite a bounce back in exploration activity in 2018, success rates and discovered volumes have dropped, according to a report by UK-based analysts Weestwood Global Energy Group.

Westwood’s 10th annual State of Exploration report reviews global conventional exploration over the last five years and looks ahead at the prospects for 2019.

It says global exploration drilling is on the rise after the cutbacks triggered by the 2014 oil price crash and the lows in activity reached in 2017. In the downturn, success rates had increased, as companies high graded their portfolios to ensure that only the best prospects were drilled. But, this didn’t last, and 2018 saw discovered volumes, average discovery size and success rates all decline, says Westwood.

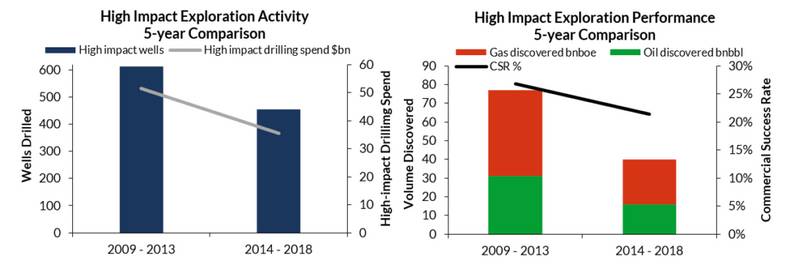

Discovered volumes from high impact drilling fell overall by 50% in the 2014-2018 period, compared to the previous five years. "Only a little over half of the decline can be accounted for by a lower well count which fell by 28%; falling success rates and average discovery sizes accounted for the rest," says Westwood. "Portfolio renewal has become a critical issue for the industry and larger companies have responded by trying harder to open new plays through increased frontier drilling.

"With oil companies planning to increase exploration drilling in 2019, the question is whether the global drilling portfolio for both near-field and high impact prospects is strong enough to sustain an increase in activity without sacrificing exploration performance," adds the company.

The State of Exploration Report looks at the last five years' global conventional exploration performance, together with exploration drilling plans for 2019. Exploration performance trends were analysed using a benchmark group of 36 international exploration and production companies that participated in 756 conventional wildcat wells between 2014 and 2018, drilled at a cost of $28.3 billion and discovering 22.4 billion boe.

Key conclusions included:

In 2018, the industry pursued a twin-track exploration strategy, increasing short cycle infrastructure-led exploration (ILX) drilling in mature plays by 40%, whilst maintaining a 65-well high impact drilling program with a greater emphasis on high impact frontier drilling, increasing frontier play tests to 29 wells from 22 in 2017. Exploration drilling activity increased by nearly 30% overall in 2018 compared to 2017.

Total commercial volumes from high impact drilling decreased to 5.4 billion boe from 9.4 billion boe in 2017 due to smaller average pool sizes, although more 100 million boe+ discoveries were made. Overall commercial success rates were down to 33% in 2018, from 48%, reversing a three-year rising trend due primarily to lower ILX success rates from a higher well count. Exploration drilling-only finding costs remained below $1/boe.

The search for new frontier plays remains a challenge and the commercial success rate for frontier exploration over the last five years has been just 6%, opening nine new plays from 154 wells at a cost of $11 billion. Two new plays were opened in 2018 but these were both in the same block as the last significant frontier discovery, in Guyana. Recent emerging oil plays appear to have limited “running room” with only the Guyana plays indicating the potential to exceed 5 billion bbl.

The continuing large gap between technical and commercial success rates in very high- risk wells points to a persistent over estimation of volumes pre-drill, with only 15% of discoveries over the last five years in the very high-risk category being deemed commercial. Few companies with significant levels of production have been able to replace produced reserves by exploration alone.

In 2019, high impact drilling is forecast to increase by 20% to around 80 wells, with more high impact wells planned in maturing and mature plays, especially in northwest Europe and Mexico. Total is leading the way with high impact wells in 2019 planning at least 20 wells. Frontier drilling is being maintained at around 30 wells. High impact exploration had already delivered 2.4 billion boe by the end of Q1 2019 and the total risked drill-out for 2019 is potentially 40% higher than the volume discovered in 2018.

Subscribe

Subscribe