The outlook for West Africa’s offshore oil and gas market remains positive despite some hiccups hinged on delay by some countries in the region to align their hydrocarbon regulations to prevailing market trends and the intensifying global competition for a share of international oil companies’ planned capital expenditure for deep- and ultra-deepwater resources.

Despite the post-2014 growth pressures on the back of fast-falling global oil prices, a number of West African offshore projects, though delayed, were kept alive partly by an emerging trend of governments in the region committing to not only change their petroleum codes to attract more private investments, but also restructure their governance structures and embrace policies that support growth of free market economies.

Currently, leading West Africa oil and gas market players such as Nigeria, Angola, Ghana, Senegal, Equatorial Guinea, Mauritania, Guinea Bissau and Cameroon have several offshore projects that are already online, being implemented or approved for implementation by international exploration and production joint ventures or in partnership with national oil companies or domestic private firms.

“Investment in offshore production is on the rise in West Africa,” says Olumide Adeosun, Director, PwC Advisory & Strategy Consulting.

“In Nigeria, Total’s Egina, one of the world’s largest floating production storage and offloading units (FPSO) came online at the end of 2018 and is expected to have a maximum output of 200,000 barrels per day (bpd). In Ghana, Eni recently contracted Yinson to convert an FPSO at a Singaporean shipyard for production and processing of oil in the country,” he said.

“With similar purchases and conversions planned in Nigeria, Ghana, Senegal and Equatorial Guinea, it is expected that the West African market will prove to be an increasingly attractive export location for FPSO expertise and services, to be rendered by international partners,” Adeosun added.

Global oil and gas exploration and production companies such as ExxonMobil, Total, Tullow, Kosmos and Oryx Petroleum have, through joint ventures with participation of national oil entities in West Africa, led in the highly expensive search for oil and gas in the region’s deep and ultra-deep waters.

Angola’s Kaombo project, in ultra-deepwater Block 32, is one of Africa’s biggest hydrocarbon investments operated by Total SA, with a 30% stake and would most likely impact performance of the region’s offshore oil and gas market in the short to long term.

“Kaombo is twice as big as any previous Total oil project in the Gulf of Guinea,” said Cyril de Coatpont, Kaombo Project Director.

“We are going deeper – from 1,400 to 1,950 meters – and we are going further – 200 kilometers farther offshore. It is our largest development to date, covering an area nearly eight times the size of Paris,” Coatpont said.

Kaombo is linked to two FPSO units, Kaombo Norte and Kaombo Sul, through 300 kilometers of subsea pipelines with Total projecting production of 230,000 bpd in 2019.

The French oil major is also proceeding with the Egina oilfield project 130 kilometers off the coast of Nigeria at water depths of more than 1,500 meters and which the company says is “one of our most ambitious ultra-deep offshore projects.” Further, the Egina project is based on a subsea production system connected to an FPSO which Total calls “the largest one Total has ever built.”

“Egina will significantly boost [Total’s] production and cash flow from 2019 onwards and benefit from our strong cost reduction efforts in Nigeria where we have reduced our operating costs by 40% over the last four years,” said Arnaud Breuillac, Total’s President Exploration and Production in the company’s 2018 annual report. The project produces 200,000 bpd, equivalent to 10% of Nigeria’s total production.

Elsewhere in Nigeria, ExxonMobil, trading as Esso Exploration Production Nigeria, is developing the Erha and Erha North projects in water depths of 1,000 meters and 1,200 meters within OML 133 license, which consist of 32 subsea wells that are tied back to an FPSO with storage capacity of 2.2 million barrels of oil and designed oil processing capacity of 210,000 bpd. ExxonMobil is the operator with a 56.25% participating interest with Shell Nigeria Exploration & Production Company (43.75%) as a partner.

As part of its 2019 work schedule, ExxonMobil has been preparing to recommence drilling in the shallow water blocks with an estimated daily production of 130,000 net oil-equivalent barrels with at least two rigs already under contract and mobilized.

ExxonMobil is pushing through more projects across in Mauritania where in 2018 the company acquired what it said was “largest ever proprietary seismic survey over blocks C14, C17 and C22.”

Through its affiliate ExxonMobil Exploration and Production Mauritania Deepwater Ltd, which owns 90% stake in the assets, the oil major looks forward to full monetization of the hydrocarbon resources in this area that covers 8.4 million acres in water depths of between 1,000 meters and 3,500 meters. But this will come after the evaluation of the blocks using 2D seismic data of nearly 6,500 kilometers and about 21,000 square kilometers of 3D survey work that is expected to continue for the better part of 2019.

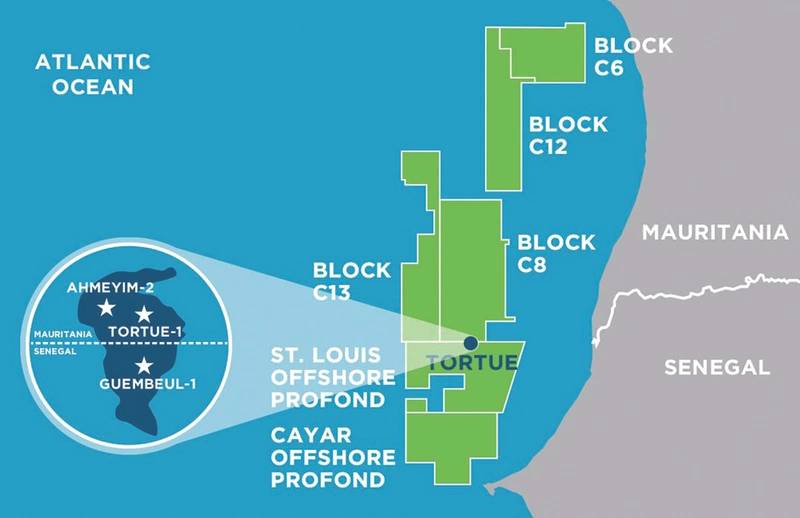

Another key achievement for the West African offshore oil and gas market was the settlement of the maritime dispute between Senegal and Mauritania that had held back the progress of the Greater Tortue Ahmeyim liquefied natural gas (LNG) project.

In December 2018, BP announced final investment decision (FID) for the project after what it said was “the agreement between Mauritania and Senegal governments and partners Kosmos Energy and national oil companies of Petrosen and SMHPM for Senegal and Mauritania respectively.

The Greater Tortue Ahmeyim project “will deliver revenues and gas to Africa and beyond for decades to come,” said Bernard Looney, BP’s Upstream Chief Executive. “We see this as the start of a new chapter for Africa’s energy story.”

The project, which is the first major one to reach FID in the basin and was initially slated to commence in the first quarter of 2019, entails producing gas from an ultra-deepwater subsea system and mid-water FPSO vessels, “which will process the gas, removing heavier hydrocarbon components before the gas is transferred to floating LNG (FLNG) facility on the maritime Senegal/Mauritania border.” The FLNG has capacity of 2.5 million metric tons of LNG/year with the first gas expected in 2022.

Map of Greater Tortue project area (Image: Kosmos Energy)

Map of Greater Tortue project area (Image: Kosmos Energy)

Other offshore oil and gas projects that are likely to drive exploration and production investment trends in West Africa include the Celba field and Okume complex, in Equatorial Guinea by Kosmos Energy’s affiliate Kosmos Equatorial Guinea, alongside exploration blocks EG21, EG24, 5 and W.

On the Senegal/Guinea Bissau border Oryx Petroleum says it is “pursuing a carbonate edge play type in AGC Central, a play type that other operators have pursued with success elsewhere in Casamance sub-basin.”

Currently, Tullow Oil is reporting good performance of the Tweneboa, Enyenra, Ntomme (TEN) offshore fields in Ghana with gross production having averaged 64,500 bpd with projections the output will surge to 73,000 barrels per day in 2019.

The deepwater project, the second biggest in Ghana after the Jubilee development, includes the use of an FPSO, John Evans Atta Mills, which has a facility with capacity to produce 80,000 bpd. The FPSO’s first oil was delivered in 2016, through subsea infrastructure across the hydrocarbon-rich field.

But whether West Africa will continue attracting additional offshore oil and gas investments will depend largely on trends in global oil prices that for long have determined exploration and production spending globally.

“West Africa will get a share of the increased spending,” predicts Jim McCaul, head of International Maritime Associates and World Energy Reports. “But exploration and production companies, particularly the big ones that operate globally, have choices as to where they spend capex resources.”

He said for West Africa to effectively compete for a share of this much needed offshore investment, governments in the region must address concerns surrounding royalties and taxation policies and local sourcing requirements on new oil and gas projects.

“Big drivers for West Africa oil and gas production are exploration and production company capex budgets, oil and gas opportunities elsewhere, government take of production revenues, political stability and stable government rules and policies,” McCaul said.

West Africa’s deepwater projects must compete for investment resources against upstream development opportunities in countries such as Guyana, Brazil and the US, McCaul said. “The biggest constraint on exploration and production spending in West Africa is existence of better opportunities elsewhere.”

“Any policy that extracts more share of revenue for the government or adds cost to the project discourages exploration and production activity,” he explained.

“The exploration and production operator will obviously prefer a deal that provides more share of the field revenue, and governments need to balance their desire to get more share of the revenue from leases, concessions, production sharing agreement, with the likelihood of discouraging new production starts,” McCaul said.

According to Adeosun, government regulation remains one of the major constraints to the growth of oil and gas in West Africa. “For example, in Nigeria, the Petroleum Industry Bill (PIB) has been held up from being passed for over a decade,” he observed.

He said, “The passage of various elements of the bill is expected to provide an improved regulatory structure for oil and gas activities, leading to increased FIDs being taken in the country, due to improved investor confidence.”

But not all West African oil and gas markets are in limbo on regulatory framework matters if the progress in Ghana is anything to go by.

Ghana, which passed its Petroleum Production and Exploration Bill in 2016, is already considering the bill for review, according to Adeosun.

“An example of a difference in regulation is the requirement for oil mining license holders in Ghana to have the capacity to develop the blocks they hold,” Adeosun said, adding that market analysts have observed hydrocarbon production more than doubled in Ghana between 2016 and 2018 since the passage of the bill.

“Another major constraint that is specific to Nigeria is pipeline vandalism and sabotage in the Niger Delta region, where most of the country’s oil and gas is produced,” he added.

Despite some West Africa oil and gas producers predicting increased offshore investment driven by recovering global oil prices, Adeosun sees little impact of this surging oil prices on planned but yet to be developed deep- and ultra-deepwater projects in the region.

“Recovering prices are unlikely to have a major impact on deep offshore projects in the short term as these projects are very highly capital intensive,” he said.

“Short term price gains will provide an initial validation for projects that have already been committed to, but not necessarily for pending projects,” Adeosun added.

In the medium to long term, however, a continued rise in the price of oil is likely to incentivize exploration companies to sign off on a higher number of FIDs.

Subscribe

Subscribe