2023 has been another noteworthy year for the rig market’s ongoing recovery, with a 3% increase in global marketed utilization versus 2022, a demand increase of 29 rigs, a 7% uptick in average contract duration, 16 further reactivations and newbuild deliveries, and not to mention floating rig dayrates exceeding the ‘magical’ $500,000 mark. So, what can we expect in 2024? Westwood has set out its top three predictions for the year ahead.

1.Some white space in 1H but further overall utilization growth

Westwood’s overall outlook for the offshore rig market remains highly optimistic, albeit with the potential for more availability during the first half of 2024.

In addition to current warm-stacked supply with no future work in place, including 27 jackups, three drillships and eight semisubmersibles (semisubs), there are another 18 jackups, four drillships and five semisubs that are currently working and set to roll off hire in the first quarter of next year alone (these figures do not include rigs that have contract options available).

Of course, for semisubs in the UK and Norway, the most active region for this rig type, the winter period generally slows down as operators try avoiding weather related downtime, but drillships are also showing more potential availability than has been recorded since September 2021. It is likely that most, if not all, of these ships with upcoming availability are being bid on new opportunities and some are likely close to securing new deals.

In the jackup segment, the majority of rigs showing upcoming availability are located in Mexico, the Middle East or Southeast Asia and several are likely to be awarded extensions with incumbent operators come the new year.

Overall this is expected to be a short-term fluctuation until operators firm up their 2024 budgets and drilling plans. Since many are now making bigger commitments for longer duration contracts, as indicated in our last Offshore Engineer article ‘Operators Offering 15-year Rig Deals as Availability Dries Up’, this can take more time to choose the most suitable rig and execute a deal.

RigLogix currently records a total of 22 tenders, pre-tenders or direct negotiations out in the market with a start date in 2024 that have a firm duration of two to five years, and many of these come with several more years of options attached to them. If also including those with start dates in 2025 and 2026, this figure increases to 46 pieces of work with some that could last as long as 10 years.

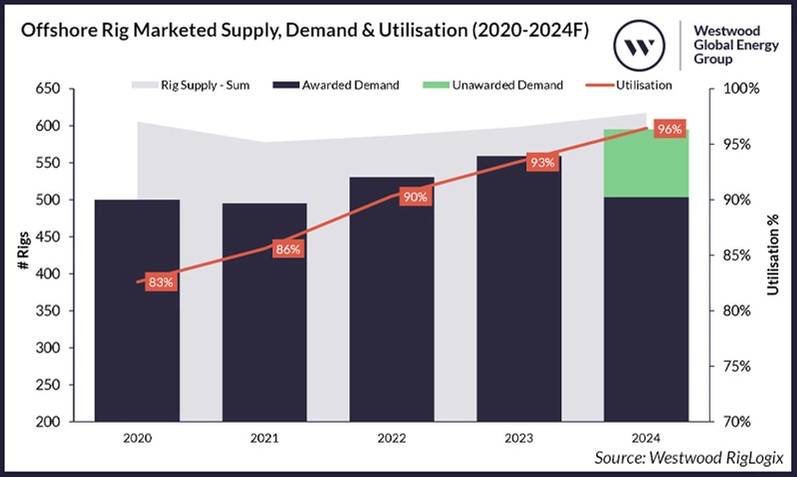

Subsequently, Westwood predicts further growth in demand and utilization next year with India, Southeast Asia, South America and West Africa all expected to be important drivers behind further expansion. This is forecast to result in demand growth of up to 36 rigs year-on-year and a 3% increase in global marketed utilization. Offshore Rig Marketed Supply, Demand & Utilisation (2020-2024F). Source: Westwood RigLogix.2.Little Attrition and Further Supply Growth

Offshore Rig Marketed Supply, Demand & Utilisation (2020-2024F). Source: Westwood RigLogix.2.Little Attrition and Further Supply Growth

As stated in our earlier Offshore Engineer article ‘Rig Dayrates Have Risen, So Where Are All The New Rig Orders?’, Westwood does not expect a wave of new construction orders in the new year, as drillers continue to focus on financial prudence. However, it is likely that further supply will be added through reactivations and newbuild rig deliveries, which offers a more economically practical option in the short term.

With the anticipated increase in demand next year, and even with some expected higher availability in the first half of the year, marketed utilization is forecast to reach as high as 96%. This will result in a limited choice of rigs for new deals, which could lead to more sublet activity and/or potential delays to planned campaigns if additional units are not added to active supply.

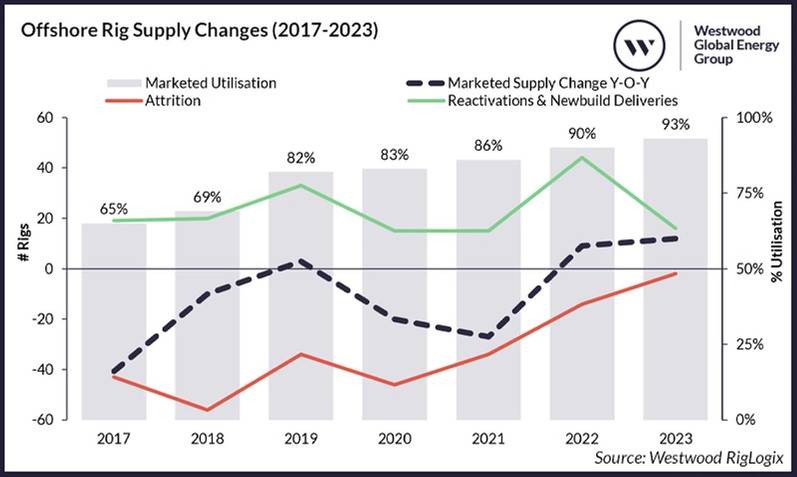

The number of reactivations and newbuild deliveries decreased by 64% this year in comparison to 2022, which is majorly attributed to national oil companies (NOCs) in the Middle East having sated their near-term jackup appetites after a contracting feast as part of a bid to ramp up domestic supply and production. Though floating rig reactivations and deliveries also decreased year-on-year, again this was mostly attributed to Brazilian NOC Petrobras cutting its award activity by 50% after a slew of long-term deals made in 2022.

Offshore Rig Supply Changes (2017-2023). Source: Westwood RigLogix.

Offshore Rig Supply Changes (2017-2023). Source: Westwood RigLogix.

However, this is expected to be short lived with Petrobras in the market with several long-term floater tenders that should result in three to four further rigs on their books, meanwhile ONGC many need as many as six more jackups next year, not to mention anticipated increased jackup activity in Southeast Asia and floating rig demand in West Africa.

Companies such as Valaris and Borr Drilling have already announced plans to take delivery of newbuild rigs, some of which have been delayed in yards for as long as a decade. It is probable that newbuilds and stranded assets will continue to be highly sought after in the new year, due to their modern and high-tech caliber. There are still 16 jackups, five semis and 11 drillships in shipyards with no contracts yet in place.

There are 86 cold stacked rigs in total, of which 39 have been idle for over five years, only eight have a five-year Special Periodic Survey (SPS) in place and 40 are already over 40 years old. Despite this, according to Westwood analysis, approximately 14 jackups, 12 drillships and 12 semis could be reactivation candidates. However, inflation and supply chain constraints have brought longer shipyard times and higher costs associated with restarting a rig, therefore this is not an easy or quick fix for supply concerns.

The lower attrition that has been recorded in 2023 (just two rigs removed from the market) will likely continue into next year too, as rig owners hold onto older units in hopes they may eventually be put back to work, especially since little to no new rigs are being built.

3.Dayrates to Continue North – but don’t expect to see all Floater Fixtures at $500,000

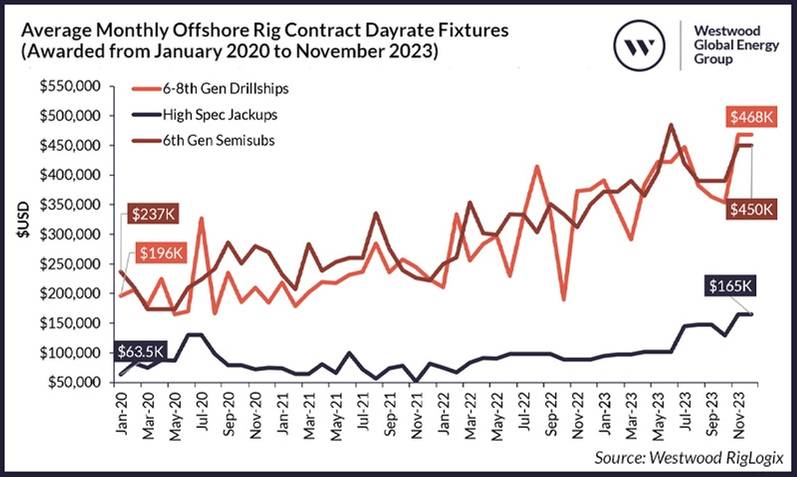

This year has brought with it continued increases in dayrates for jackups, semisubs and drillships – with the latter two floating rig types now both having witnessed clean dayrates (excluding additional services such as MPD or mobilization) at or above $500,000 per day.

These market leading rates are a positive sign, especially for rig owners and managers that have grappled with low dayrates since 2014. However, this is unlikely to be the norm for long-term contracts starting in 2024. The majority of fixtures in 2023 with dayrates that fell between $480,000 to $500,000 per day were for relatively short-term deals (i.e. 1-2 wells, 30 -200 days) or do not begin until 2025 onwards.

Next year Westwood expects a continued variance in floater dayrates with some long-term deals that could still be fixed in at the mid-to-high $300,000s as well as short-term deals that we expect will further exceed those leading rates already witnessed this year.

Meanwhile, the jackup segment has now seen a contract fixed with a dayrate of $180,000 for work off Australia, while two contracts have been fixed at over $165,000 per day for work in Southeast Asia. As is the case with the floating rig segment, Westwood forecasts to see more upward movement next year in line with the forecast tight market, but a likely continued range of rates based on term, location and technical specifications.

Average Monthly Offshore Rig Contract Dayrate Fixtures (Awarded from January 2020 to November 2023). Source: Westwood RigLogix

Average Monthly Offshore Rig Contract Dayrate Fixtures (Awarded from January 2020 to November 2023). Source: Westwood RigLogix

Ultimately, with the ever-tightening supply/demand balance, costly reactivation and new construction economics as well as inflationary pressures, Westwood expects dayrates to continue their northward trajectory in 2024 across the board. With that in mind, we predict that operators will continue locking in rigs earlier for their contracts in a bid to secure the right assets at as low a price as possible.

Subscribe

Subscribe